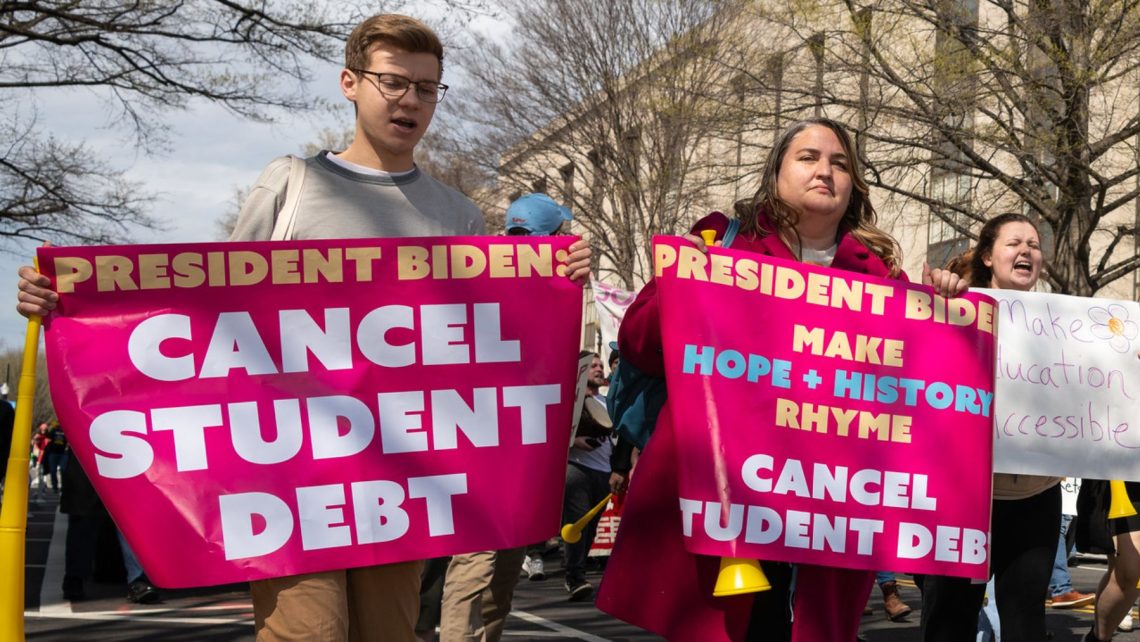

Starting in the fall of 2024, thousands of people who have seen the interest on their student loans accumulate and multiply could get a forgiveness of these financial obligations thanks to a plan proposed by the administration of the Joe Biden administration. The main requirement is to earn $120,000 or less a year to be one of the beneficiaries of this ambitious plan, which is part of a larger project of the Biden administration to help highly indebted students.

If approved, millions of borrowers who meet certain criteria would be able to access this benefit, which could greatly ease their finances. The goal is to provide the long-awaited relief for those who have seen their debts increase over time due to interest.

With interest rates on federal student loans hitting record highs this summer, debt relief based on interest accrual would be great news for many borrowers. Here we explain more about how this plan works.

Why Are Thousands Under the Water With Their Student Loans?

Most federal student loan debt is unsubsidized, which means the government doesn’t cover the interest while you’re in school or grad school. As a result, when you start repaying, you owe more than you originally borrowed due to the accumulation of interest.

Some repayment plans may even cause borrowers to be overwhelmed by interest. Gradual repayment plans, for example, start with payments that only cover interest for the first few years, and a small part of the money that is contributed monthly reduces the debt. This means that you can make important payments without even reducing the total balance. In addition, many borrowers on income-based plans have seen their balances increase because their payments are not enough to cover all the accumulated interest.

During deferment or forbearance periods, most federal student loans continue to accrue interest. Many people use these programs when they have difficulty paying, not knowing that there are other options available, such as income-based plans.

Your Due Interests Could Turn to Debt, and That’s BAD

In addition, certain events can trigger interest compounding, which means that the accumulated interest is added to the main balance of the loan. You understand what this means, right? That these accumulated interests become a balance owed that in turn will generate new interest. Situations such as coming out of an indulgence, changing payment plans or not recertifying income for an income-based plan can cause this compounding.

Student loan forgiveness for borrowers with high accrued interest

Under Biden’s proposed Loan Forgiveness Plan, many borrowers would see partial or full interest relief on their balances, as long as they had increased due to the accumulation of interest.

All federal borrowers could get up to $20,000 in student loan forgiveness if they have accrued or capitalized interest since they started repaying.

There’s also good news for low-income borrowers: They could get even more relief. Single or married borrowers who file taxes separately could receive full forgiveness of their accrued or capitalized interest on loans if they earn $120,000 a year or less, and are enrolled in an IDR plan, such as Biden’s SAVE plan.

Those borrowers who file taxes as the head of household could get the same relief, but they need to earn $180,000 or less per year. Married borrowers who file taxes jointly with their spouse may be eligible if they earn $240,000 a year or less.

Other Initiatives for Student Borrowers

This is not the only initiative that is being carried out all over the United States to help people who are submerged underwater with accumulated interest or interest compounding. There’s also the SAVE plan, Biden’s newest option for income-based payment, known as IDR. This project offers interest forgiveness on student loans that exceed the borrower’s monthly payment.

It is worth clarifying that this does not eliminate the growth of the past balance due to negative amortization, but it will prevent the borrower’s balance from continuing to increase for that particular reason.

Last year, the Biden administration also introduced regulatory reforms to eliminate various interest compounding triggers, such as exiting an indulgence, certain IDR plans, defaulting on a payment or failing to update income information. This does not stop the accumulation of interest, but it will reduce the compounding effect of compounding, thereby preventing the balance from increasing significantly over time.